.avif)

I've been watching the Netflix-Warner Bros deal unfold, and something struck me immediately.

This isn't just an entertainment story.

Netflix just spent $72 billion to acquire Warner Bros Discovery's film and streaming businesses. They're getting Harry Potter, Game of Thrones, HBO Max, and a century-old content library. The deal emerged after a competitive bidding process and won't close until 2026, pending regulatory approval.

But here's what matters for SaaS founders: the strategic patterns driving this consolidation mirror exactly what's reshaping the SaaS market right now.

Netflix surpassed 300 million global streaming subscribers at the end of 2024. Warner Bros Discovery adds another 128 million. Combined, they'll control 56% of mobile app monthly active users in global streaming.

Sound familiar? SaaS M&A increased more than 41% in 2024 compared to 2023. SaaS transactions made up 61% of all software M&A activity last year.

Scale isn't optional anymore. It's survival.

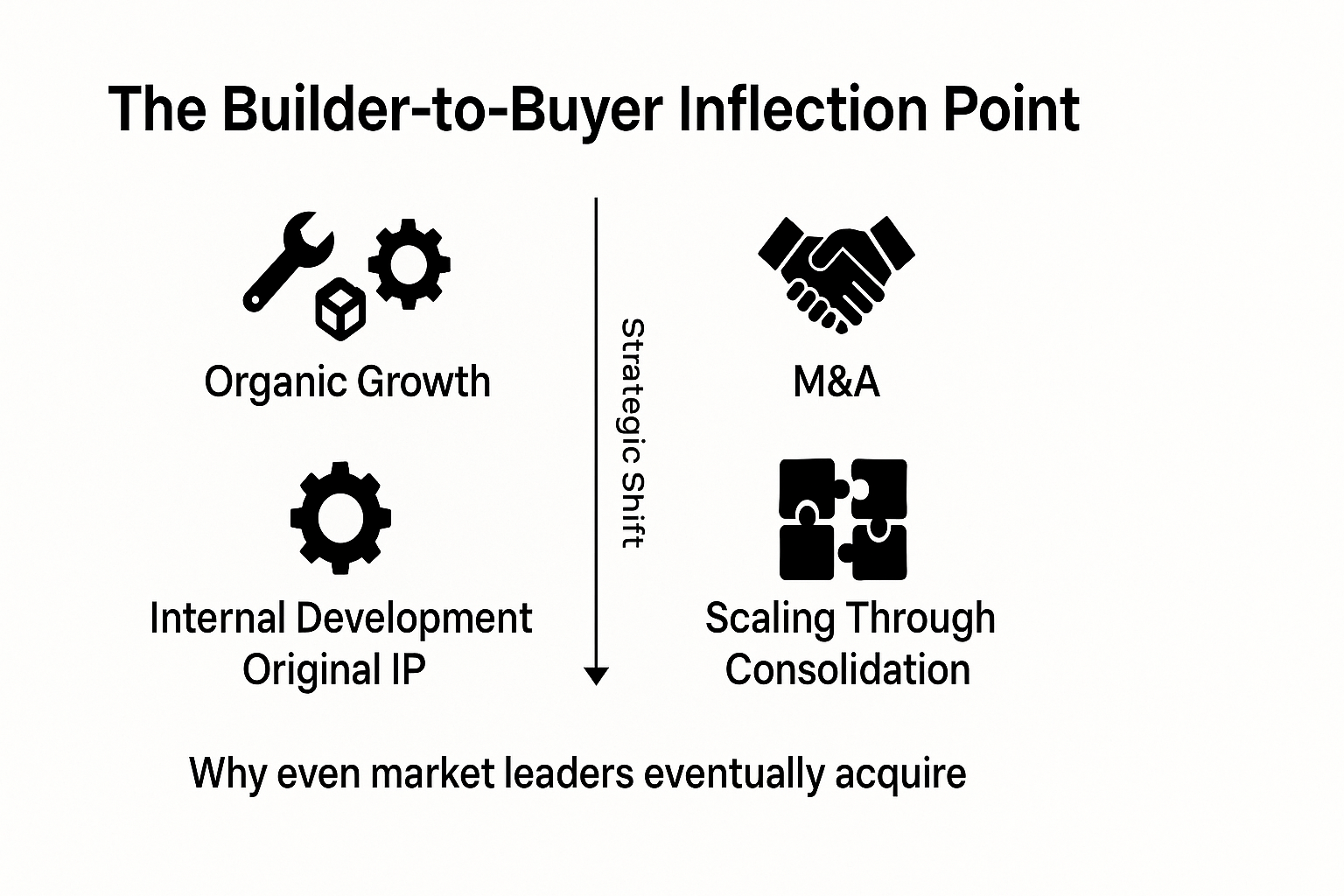

When Builders Become Buyers

Netflix has always been a builder. They've never executed a major acquisition. They leaned into developing their own intellectual property, creating original content, building infrastructure from scratch.

Until now.

This $72 billion deal represents a complete strategic pivot. Even the most successful companies eventually hit a ceiling where organic growth can't deliver the competitive advantage they need.

I see this pattern playing out across SaaS right now.

Private equity investors drove 61% of all SaaS transactions through platform acquisitions in 2024. Strategic buyers accounted for 39% of total deals. Companies that once prided themselves on organic growth are actively pursuing M&A to capture market share faster than competitors can respond.

The builder-to-buyer transformation isn't a failure. It's a recognition that market dynamics have fundamentally changed.

You can build the best product in your category and still lose if someone consolidates the market around you. Netflix understood this. They watched competitors merge, acquire, and consolidate. They realized that continuing to build organically meant accepting a permanent disadvantage in content library depth.

The Economics of Market Concentration

Netflix currently claims 46% of mobile app monthly active users in global streaming. Add HBO Max, and that share rises to 56%.

That level of market concentration changes everything about pricing power.

Firms with monopoly power can charge higher prices because demand becomes relatively inelastic. When you control the majority of premium content, subscribers have fewer alternatives. You're not competing on price anymore—you're extracting value from market position.

This dynamic is reshaping SaaS pricing strategies right now.

As fewer players control larger market shares, they gain the ability to optimize pricing in ways fragmented markets cannot support. Median EV/TTM revenue multiples for SaaS companies increased from 3.8x to 4.0x in 2024, with in-quarter multiples reaching 5.7x.

Buyers are paying premiums for businesses that demonstrate pricing power through market position.

If you're building a SaaS company in healthcare, finance, or technology verticals, you need to think about this carefully. Market concentration isn't just about revenue growth—it's about fundamentally restructuring the economics of your category to capture pricing power that fragmented competitors can't access.

The $2-3 Billion Efficiency Play

Netflix projects $2-3 billion in cost savings through operational consolidation. They're eliminating redundancies between their operations and Warner Bros—duplicate overhead, redundant technology stacks, overlapping administrative functions.

This efficiency-first approach mirrors what's driving SaaS consolidation.

The streaming deal values Warner Bros at an enterprise value exceeding its market capitalization. Acquirers are willing to pay premiums for assets that deliver immediate operational synergies.

I see SaaS buyers making the same calculation.

When you can demonstrate clear integration pathways and quantifiable cost synergies, you make your business exponentially more attractive to strategic acquirers and PE buyers. They're not just buying your revenue—they're buying the ability to consolidate technology stacks, eliminate duplicate overhead, and achieve economies of scale.

This validates a critical Go-To-Market strategy: build your business to be integration-ready.

Document your technology architecture. Map your operational processes. Identify where your systems overlap with potential acquirers. The companies that can articulate exactly how they'll generate $X million in cost savings within 12 months of acquisition command premium valuations.

Vertical Integration and the End-to-End Solution Premium

If regulators approve this deal, Netflix will unite the world's largest streaming destination with a 102-year-old film studio. They'll own content creation, distribution infrastructure, and the platform itself.

This vertical integration strategy commands premium valuations because it eliminates dependencies.

Warner Bros' portfolio includes HBO, HBO Max, and franchises like Harry Potter. Netflix gets end-to-end control over how that content is created, distributed, and monetized. They're not licensing content anymore—they're owning the entire value chain.

The same dynamic is reshaping SaaS valuations.

Vertical integration enables companies to offer comprehensive solutions that boost operational efficiency. The shift toward cloud-based programs, now at 70%, marks a major change in how businesses operate.

SaaS companies that demonstrate end-to-end solutions rather than point solutions capture disproportionate value in M&A markets.

If you're building in a specific vertical—healthcare, finance, technology—expanding beyond a single product to create integrated workflows dramatically increases your strategic value. Buyers pay premiums for platforms that reduce their customers' need to stitch together multiple vendors.

The Regulatory Wildcard

Netflix agreed to pay a $5.8 billion breakup fee to Warner Bros Discovery if the government blocks the deal.

That's massive execution risk.

The deal won't close until 2026, pending regulatory approval from competition authorities. The Writers Guild of America has already called for the merger to be blocked, arguing it will eliminate jobs, suppress wages, reduce content diversity, and raise consumer prices.

This regulatory uncertainty is increasingly relevant for SaaS companies.

The acquisition of SaaS companies witnessed a sharp 23% decline in 2022 due to market conditions. Scrutiny of tech consolidation continues to intensify. Regulators are asking harder questions about market concentration, pricing power, and competitive effects.

For SaaS founders considering M&A—either as buyers or sellers—understanding regulatory pathways is becoming table stakes.

Companies that proactively address market concentration issues, demonstrate consumer benefits, and structure transactions intelligently will have significant advantages in completing deals successfully.

Warner Bros' strategic decision to separate its business units before sale demonstrates this principle. They retained cable networks while divesting streaming assets, potentially reducing antitrust concerns about excessive market concentration.

The Mature Market Signal

Netflix's willingness to spend $72 billion on acquisition rather than continuing its builder strategy signals a fundamental market maturity shift.

The global video streaming market was estimated at $129.26 billion in 2024 and is projected to reach $416.8 billion by 2030, growing at a 21.5% CAGR.

Despite this growth trajectory, Netflix chose consolidation over organic expansion.

This mirrors SaaS market dynamics where cooling inflation and Federal Reserve interest rate cuts heading into 2024 enhanced transaction volumes. Global IT spending surpassed $5 trillion and enterprise software surpassed $1 trillion for the first time.

Even in high-growth markets, the path to dominance increasingly runs through strategic M&A rather than pure organic growth.

I see founders preparing their businesses for growth without considering eventual consolidation. That's a mistake. You should be building your business not just for growth, but for eventual consolidation—either as an acquirer or an acquisition target.

This means different things depending on your stage:

Early stage: Document everything. Build clean systems. Make your business intelligible to potential acquirers.

Growth stage: Identify integration synergies with potential acquirers. Understand where you fit in consolidation scenarios.

Scale stage: Develop acquisition capabilities yourself. Build the infrastructure to integrate acquired companies.

What This Means for Your Go-To-Market Strategy

The Netflix-Warner Bros deal reveals patterns that directly impact how you should think about building and positioning your SaaS business.

Market consolidation is accelerating. Scale advantages are compounding. The companies that recognize these dynamics and build accordingly will capture disproportionate value.

Here's what I'm watching:

Positioning for strategic value. Build your business to be acquisition-ready from day one. Document your technology architecture, operational processes, and integration pathways. Buyers pay premiums for businesses they can integrate cleanly.

Vertical integration advantages. Expand beyond point solutions to create end-to-end workflows in your target vertical. Healthcare, finance, and technology buyers want platforms that reduce vendor fragmentation.

Efficiency as a value driver. Demonstrate quantifiable cost synergies. Show exactly how an acquirer will generate $X million in savings within 12 months of acquisition.

Regulatory awareness. Structure your business and potential transactions to address competition concerns proactively. Companies that navigate regulatory pathways successfully have significant advantages.

Market timing recognition. Understand where your market sits in the consolidation cycle. Early-stage markets favor organic growth. Mature markets favor strategic M&A.

Netflix spent 15 years building organically before making this acquisition. They recognized when market dynamics shifted from growth to consolidation. They adapted their strategy accordingly.

You need to do the same.

The Consolidation Imperative

Netflix's $72 billion acquisition of Warner Bros isn't just an entertainment story. It's a signal about how markets mature and how winning companies adapt.

The streaming wars are over. The consolidation phase has begun.

SaaS is following the same pattern. M&A activity increased 41% in 2024. Private equity and strategic buyers are actively consolidating fragmented markets. The companies that recognize this dynamic and position accordingly will capture disproportionate value.

The question isn't whether consolidation will reshape your market. The question is whether you'll be positioned to benefit from it.

Build for scale. Document for integration. Position for strategic value.

That's how you win in consolidating markets.

About the Author

.svg)

.svg)

.png)

.png)

.png)

.jpg)

.jpg)